Blockchain technology has quickly become a hot topic in many societal realms, as from finance to healthcare, or gaming to supply chain management, the tech has the potential to transform the way we live, work, and entertain ourselves.

However as of 2024, many people are still unfamiliar with the basics of blockchain technology, and how it operates in practice. This beginner’s guide therefore aims to break down the tech’s key concepts in a simple and easy-to-digest manner, so that you can grasp the fundamentals without scratching your head too much.

It will also include links to other articles that explore different areas of blockchain technology in more depth.

What Is Blockchain Technology

A blockchain is like a digital ledger that records transactions in a secure, transparent, and tamper-proof manner. You can imagine one as a chain of interconnected blocks, where each block contains information about transactions, ownership, and other valuable data.

While most widely recognised for their role in facilitating cryptocurrencies – where they maintain a secure and decentralized record of all transactions – blockchain applications can extend way beyond this.

This is because their primary function lies in rendering immutable data, signifying that once a new block is generated and data is entered into it, it becomes resistant to any alterations, as well as unable to be changed or tampered with. That being said, entire blockchains can be split into a new competing path in a process known as forking.

The inability to change or tamper with data is a unique feature that minimizes the need for trust to be distributed throughout the entire system – as trust is only required at the point wherein data is initially entered by a user base or program. Therefore, the immutability of data within blockchains is one of the main benefits of Blockchain technology, as reductions in reliance on trusted third parties, such as auditors or humans prone to errors, leads to increased transparency and lower operational costs.

A Brief History of Blockchain Technology

David Chaum proposed the idea of blockchain-like protocols in 1982, in his dissertation titled ‘Computer networks established, maintained, and Trusted by Mutually Suspicious Groups.’

By 1991, computer scientists Stuart Haber and Scott Stornetta continued research on the topic, and together with Dave Bayer, they introduced Merkel’s tree designs into blockchain technology, as a form of incorporating several data entries into one block.

Bitcoin, the world’s first blockchain, was then developed in 2008 by pseudonymous individual Satoshi Nakamoto – with Haber and Stornetta being the most cited sources within the Bitcoin Whitepaper.

Here, the network served as the first publicly distributed ledger to store financial transactions for the world’s first cryptocurrency, Bitcoin (BTC). By leveraging the powers of blockchain tech, Bitcoin became the first digital currency to solve the ever-troublesome double spending problem – and it did this without needing a trusted authority or central server.

How did Blockchain Technology Evolve?

Let’s take a look at the evolution of blockchain technology beyond the birth of Bitcoin.

- Blockchain 1.0 – The Age of Cryptocurrencies

The first version of blockchain technology primarily focussed on cryptocurrencies, including aspects such as currency conversion, remittances, and digital payment systems. This stage was closely associated with Bitcoin, often leading to a common misconception that Bitcoin and ‘blockchain’ are one and the same thing.

- Blockchain 2.0 – The Era of Smart Contracts & dApps

Expanding on the initial uses, Blockchain 2.0 led to the development of broader financial applications which facilitated the digital management of stocks, bonds, checks, debt, ownership records, and contractual agreements, showcasing its potential beyond mere currency transactions.

Innovations in a realm called smart contracts helped develop this, with Vitalik Buterin’s Ethereum (ETH) being today’s leading blockchain network for smart contracts and decentrally-built applications (dApps).

- Blockchain 3.0 – The Introduction of Web 3.0

The third phase of blockchain’s evolution – in which we are currently living – extends its applications beyond financial sectors into areas like education, government, healthcare, and the arts. This iteration signifies blockchain’s capacity to revolutionize traditional operations and record-keeping across various industries.

- Blockchain 4.0 – Integration with AI, IoT & Emerging Technologies

Envisioned as the future of blockchain, Blockchain 4.0 aims to synergize with advanced technologies such as Artificial Intelligence (AI) and the Internet of Things (IoT). Although not yet fully realized, this phase anticipates creating multifaceted applications across diverse sectors, potentially transforming the technological landscape forever.

In turn, Blockchain 4.0 is what could signal the onset of living in the ‘metaverse’.

Structure and Design of Blockchains

The basic structure of a blockchain consists of a chain of blocks linked together in chronological order.

Each block contains:

- Block Header: Identifies and manages each block within the blockchain; includes metadata like previous block hash, timestamp, and Merkle root.

- Data: This could be anything valuable—money, contracts, intellectual property, or even the temperature of a food shipment.

- Timestamp: The exact time when the data was added or recorded.

- A Reference to the Previous Block: This creates a continuous chain. Once a block is added, it cannot be changed or deleted, making it “immutable.”

- Nonce: A unique number used once per block in mining to meet specific network criteria; essential for blockchains which use Proof-of-Work (PoW) consensus mechanisms.

- Merkle Root: Summarizes all transactions in a block using a single hash, enabling efficient and secure transaction verification.

Blockchain Nodes

A blockchain node is a participant in a blockchain network. It can be individuals, organizations, or computers.

In essence, multiple blockchain nodes work together in order to maintain the blockchain by:

- Validation: Verifying transactions by solving complex mathematical puzzles (a process called mining).

- Consensus: Reaching an agreement on the validity of transactions – standard consensus protocols include Proof of Work (PoW) and Proof of Stake (PoS).

- Distribution: Storing a copy of the entire blockchain, ensuring redundancy and decentralization.

- Security: The more nodes, the harder it is to manipulate the blockchain.

How Does Blockchain Technology Work?

Blockchain technology operates on a decentralized network of computers, meaning there is no central authority controlling the system. To give you the best rudimentary understanding, let’s examine how a transaction works on the blockchain.

- When a transaction occurs, it is verified by multiple nodes across the network. This system keeps the blockchain safe from being altered by hackers.

- Once a user initiates a transaction, the transaction logs with other transactions in a pool called the mempool.

- Online miners/validators then pick up the transactions and drop them in a transaction block till it’s full.

- Once validated, the transaction is added to a block and linked to the previous block in the chain.

- The entire block then gets encrypted using a special algorithm, and the mining process begins. This process creates a transparent and secure record of transactions that cannot be altered.

For extra context, mining involves each miner trying to guess the hash code on the new block, in order to generate it. Here, individual miners must generate a hash code that’s greater than the block’s hash card in order to win the race. In turn, the miner with the most hash at the end of a ten-minute block mining period gets the mining reward.

What is a Blockchain Transaction?

A blockchain transaction is the process of transferring data, assets, or any valuable information from one party to another on a blockchain network. Each transaction involves the exchange of digital tokens or assets, such as cryptocurrencies like BTC or ETH.

When a transaction occurs on a blockchain, it goes through several steps, which we will explain below:

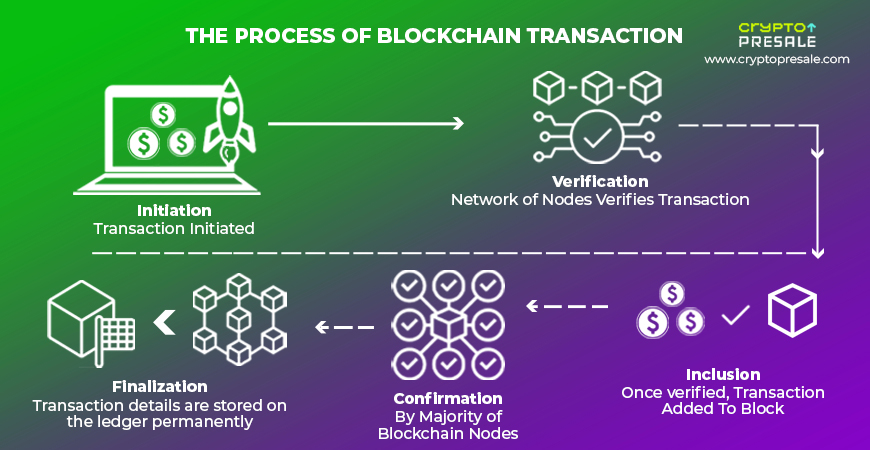

The Process of Blockchain Transactions

- Initiation: The sender initiates the transaction by creating a digital signature and specifying the recipient and amount to be transferred.

- Verification: The transaction is broadcasted to the network of nodes, where it is verified using cryptographic algorithms.

- Inclusion in a Block: Once verified, the transaction is grouped with other transactions to form a block, which is then added to the blockchain.

- Confirmation: The block containing the transaction must be confirmed by a majority of nodes in the network, ensuring its validity and security.

- Finalization: Once confirmed, the transaction is considered final and cannot be reversed or altered. The transaction details are then stored on the blockchain ledger for future reference.

Types of Blockchain Networks

Most of the commonly known blockchains for cryptocurrencies are public blockchains, allowing multiple users to access the platforms at any time and from anywhere around the world.

However, there are other types of blockchains, which are used across different sectors to perform specific functions. To explore these in more depth, visit our article on different types of blockchains – however if not, below is a brief exploration.

Public Blockchains

Public blockchains are blockchains where anyone with an internet connection can join in. Typically, they are chains designed for cryptocurrencies to be built on.

The permissionless nature allows users to store transaction data across the distributed network. In turn, this is the core principle of decentralized finance (DeFi), as these systems offer a more secure and transparent means of storing information compared to conventional centralized platforms.

Private Blockchains

Private blockchains differ from public blockchains, in that each node has to be verified before they join the network.

Therefore, they are not open source – as the verification comes at the point of entry – however this means that their security is less developed compared to public blockchains, as they contain a smaller number of nodes.

As a result, private blockchains are often on a smaller scale than public blockchains, and are better suited for companies or organizations that require a small network for their staff.

Hybrid Blockchains

There’s also something in between – the hybrid blockchain network – wherein there’s a private blockchain for storing confidential information, and a public blockchain for other users to access information.

Intuitively, this is best applied in industries such as real estate and healthcare companies, where company-specific data can be stored on the private blockchain, and public information such as ads can be stored on the public blockchain for other users to access.

Consortium Blockchains

Consortium blockchains – also referred to as federated blockchains – are similar to hybrid blockchains in that they have both private and public networks. The difference here is that consortium blockchains are best for a group of companies that need to come together to access similar information.

For example, several banks can come together to form a blockchain where each bank maintains their private network whilst interacting with the other banks on the public blockchain.

Blockchain Scalability

Blockchain scalability is a critical issue that significantly impacts the technology’s potential for widespread adoption. For context, while Visa can process up to 24,000 transactions per second (TPS), Bitcoin manages only about seven TPS. Ethereum – being a bit more robust – handles 20 to 30 TPS.

These figures highlight a stark gap between traditional financial systems and cryptocurrencies, which must be bridged for cryptocurrencies to compete effectively.

Scalability in blockchain revolves around three main factors:

- Throughput: This refers to the number of transactions a network can process per second (TPS). While high throughput is desirable, it’s not the sole factor in assessing a blockchain’s efficiency.

- Confirmation Time: This is the time it takes for a transaction to be considered secure and irreversible. For instance, a system might boast a high TPS but suffer from prolonged confirmation times, making it impractical for daily transactions.

- Finality: This is the guarantee that once transactions are confirmed, they cannot be altered or reversed. In blockchain systems like Bitcoin, achieving finality typically requires the addition of several blocks after the transaction block, which can add to the delay.

Blockchain Decentralization

Decentralization is the most fundamental principle of blockchains. As a concept, it eliminates the need for intermediaries and central authorities in transactions.

This is because in a decentralized blockchain network, information is distributed across multiple nodes or computers, with each node having a copy of the entire blockchain ledger. This ensures that no single entity controls the network, making it more resilient to censorship, manipulation, and single points of failure.

In addition to single points of failure, decentralization also reduces the risk of single point attacks – as since there is no central server or authority that hackers can target, it becomes more challenging for malicious actors to compromise the network or manipulate transaction data.

This distributed architecture ensures that even if some nodes are compromised, the integrity of the blockchain can still be maintained by the remaining honest nodes.

And although widely advertised as decentralized solutions, centralized blockchains also exist – however as their name suggests, a single entity or authority maintains control over these networks, leaving them susceptible to centrally-sourced issues such as censorship, unauthorized alterations, and security vulnerabilities.

Blockchain Interoperabi1lity

Blockchain interoperability refers to the capability of different blockchains communicating and sharing data with one another.

This multi-chain functionality is crucial for the plethora of cross-chain interactions that may come in the future, as it essentially facilitates operations on one blockchain being recognized and processed on another. In practice, this will pave the way for enhancing the utility and efficiency of dApps.

Core Mechanisms of Blockchain Interoperability

- Cross-Chain Messaging Protocols: These protocols allow blockchains to read and write data across different networks, which will prove to be essential for creating cross-chain dApps which operate across multiple blockchains by using unified logic in smart contracts.

- Token Bridges and Data Messaging: While token bridges facilitate the transfer of cryptocurrency between blockchains, more sophisticated data messaging protocols enable the sharing of various types of data, supporting complex applications like cross-chain exchanges and DeFi markets.

Importance of Blockchain Interoperability

- Enhanced Functionality: Interoperability extends the functionality of blockchains beyond their native capabilities. For example, a dApp could combine Ethereum’s smart contract capabilities with Bitcoin’s secure transaction environment.

- Unified Liquidity and Global State: By enabling cross-chain interactions, interoperability helps maintain a unified state of applications and pooled liquidity.

- Innovation and Scalability: Interoperability is key to innovation in the blockchain space, as it allows developers to build versatile and scalable solutions that can interact across multiple platforms without being limited to the capabilities of a single blockchain.

The Key Elements of Blockchains

Here are four key components of blockchain networks; the genesis block, blockchain protocols, blockchain layers, and crypto wallets.

Genesis Block

The Genesis Block (or Block 0) is the very first block in a blockchain network.

Serving as the foundation of an entire blockchain, it contains unique data that sets it apart from all other blocks. In turn, Genesis Blocks are hardcoded into blockchain protocols, and do not reference any previous blocks since they’re the starting points.

Blockchain Protocols

Blockchain protocols are the rules and guidelines that govern how a blockchain network operates. More specifically, these protocols define how transactions are validated, how new blocks are added, and how consensus is reached among participants in the network.

Two of the most common blockchain protocols include:

- Proof of Work (PoW): In a PoW protocol, miners compete to solve complex mathematical puzzles in order to add new blocks to the blockchain. This process requires a significant amount of computational power and electricity, making it secure but energy-intensive.

- Proof of Stake (PoS): In a PoS protocol, validators are chosen based on the number of tokens they hold in the network. This method proves to be more energy-efficient than PoW, whilst still ensuring security and consensus among participants.

Blockchain Layers

There are multiple layers of blockchain networks, with each serving a specific purpose to ensure the security and efficiency of the network, as well as maintain the integrity of transactions and data on the blockchain.

Below is a brief overview of the main blockchain layers – however for a more in-depth exploration on the topic, visit our article on the different layers of blockchain networks.

1. P2P Network Layer

The Peer-to-Peer (P2P) network layer is the foundation of a blockchain system, responsible for connecting all nodes in the network and facilitating communication between them. Often referred to as Layer 0 Blockchain, the P2P layer ensures that information is transmitted securely and efficiently across the network.

2. Consensus Layer

The consensus layer is responsible for ensuring that all nodes in the network agree on the validity of transactions and blocks added to the blockchain. Also known as Layer 1 Blockchain, this layer helps prevent fraud and double-spending on the network.

3. Data Layer

The data layer is where all transaction data, smart contracts, and other information are stored on the blockchain. Often called Layer 2 Blockchain, this layer ensures the integrity and immutability of data, making it tamper-proof and transparent. As of 2024, Polygon – which is built on Ethereum – is the most famous example of a Layer 2 network.

4. Application Layer

The application layer is where developers can build dApps that run on a particular blockchain network, further creating innovative solutions and blockchain use cases across various industries.

Blockchain Wallets

A blockchain wallet – also known as a crypto or DeFi wallet – is a digital tool that allows users to store, manage, and transfer their cryptocurrencies securely. There are two main types of blockchain cryptocurrency wallets:

- Hot Wallets: Hot wallets are online wallets that are connected to the internet, making them convenient but more susceptible to hacking. Examples include online exchanges and mobile wallets.

- Cold Wallets: Cold wallets are offline wallets not connected to the internet, making them more secure but less convenient for frequent transactions. Examples include hardware wallets such as Ledger and paper wallets.

For a comprehensive breakdown over crypto wallets – including their features, security capabilities, and how they work, visit our “What is a blockchain wallet” article.

Blockchain Security

Here are a few key reasons why maintaining robust blockchain security measures is so essential:

1. Protection of Assets

Intuitively, the main reason to prioritize blockchain security is to protect the digital assets that are stored in your blockchain wallet.

2. Prevent Fraud

By maintaining high levels of security, fraudulent activities such as double-spending or tampering with transaction records can be prevented, safeguarding the integrity of the network, as well as users’ assets.

3. Maintaining Privacy

Blockchain technology allows for transparent and immutable record-keeping, but it is also important to protect the privacy of users. Therefore, strong security measures help prevent unauthorized access to personal information and transaction details, ensuring that sensitive data remains confidential.

Cryptography in Blockchain Technology

Within the process of protecting sensitive information and ensuring the integrity of transactions, blockchain tech relies on cryptography.

For context, cryptography involves using mathematical algorithms to encrypt data, making it unreadable to anyone without the corresponding decryption key. This process helps secure blockchain wallets and prevent unauthorized access or tampering with transaction records.

There are several cryptography techniques used within blockchain security – one of which being public-key cryptography. In this system, each user has a pair of cryptographic keys, which consists of a public key that’s shared with others to receive funds or verify transactions, and a private key, which is kept secret and used to sign transactions. This asymmetrical encryption ensures that only the owner of the private key can access their funds and authorize transactions.

Blockchain Consensus Algorithms

Blockchain consensus algorithms are protocols that are used to achieve agreement among participants in a blockchain network, regarding whether a particular data can join the chain. Some common consensus mechanisms include:

- Proof of Work (PoW): As mentioned earlier, PoW requires miners to solve complex mathematical puzzles to validate transactions and add new blocks to the blockchain.

- Proof of Stake (PoS): In PoS, validators are chosen based on the number of tokens they hold in the network rather than computational power.

- Delegated Proof of Stake (DPoS): DPoS allows token holders to vote on which delegates can validate transactions on their behalf.

- Byzantine Fault Tolerance (BFT): BFT mechanisms ensure that the network can reach consensus even if some participants are behaving maliciously. Examples include Practical Byzantine Fault Tolerance (PBFT) and Federated Byzantine Agreement (FBA).

Blockchain Hash & Hash Functions

Blockchain hashes play a role in ensuring the security and immutability of blockchain networks.

They work via hash functions, which are mathematical algorithms that take an input (data) and produce a fixed-size output, known as a hash value or digest. This hash value uniquely represents the input data, which in turn, makes it easy to verify the integrity of information stored in a block.

Further, hash functions are used to create a unique identifier for each block in the chain. This means that when a new block is added to the blockchain, it is assigned a hash value based on its contents, including transaction data and the hash of the previous block. This hash value then serves as a digital fingerprint for the block, making it easy to detect any changes or data tamperings.

Additionally, since each block’s hash is based on the previous block’s hash, any attempt to alter a block in the chain would require changing all subsequent blocks as well, making it virtually impossible to manipulate the blockchain without detection.

On the day to day user side of things, unique hash values allow them to verify the authenticity of transactions, as well as track their history within the blockchain.

Practical Applications of Blockchains

Let’s take a look at how different industries utilize blockchain technology.

Blockchain Gaming

Blockchain technology is revolutionizing the gaming industry by introducing new possibilities for in-game assets, digital ownership, and secure transactions. This is because in blockchain-based games, players have true ownership of their in-game items and currencies, as they are stored on a decentralized ledger that cannot be manipulated or controlled by game developers.

The main advantage of blockchain gaming is the ability to trade in-game assets with other players or even across different games, creating a new economy within the gaming world. This concept of interoperability allows for unique player experiences, whilst opening up new opportunities for monetisation through the sale of rare items and digital collectables.

Additionally, blockchain technology provides a transparent and secure platform for hosting online tournaments, verifying player identities, and ensuring fair gameplay. For example, smart contracts can be used to automate prize distributions, enforce rules, and maintain the integrity of competitions.

Moreover, blockchain technology enables players to earn rewards in the form of cryptocurrency for their achievements in games, creating new incentives and monetisation opportunities for both players and developers. This approach to gaming – often known as Play-to-Earn (P2E) – has the ability to disrupt traditional models and redefine how games are played, developed, and monetised.

Day-to-Day Blockchain Applications

Below are some of the blockchain applications in our everyday life.

- Money Transfers: Blockchain technology revolutionizes money transfers, offering a faster and more cost-effective alternative to traditional services. Particularly beneficial for cross-border transactions, the tech facilitates secure transactions that are completed within minutes.

- Lending: Blockchain technology enables lenders to execute collateralised loans through smart contracts, automating events like service payments and loan repayments. This results in faster, more affordable loan processing with improved rates for borrowers.

- Insurance: Smart contracts on the blockchain enhance transparency in insurance by preventing duplicate claims and expediting payment processes. This technology ensures a secure and transparent recording of all claims, benefitting both customers and providers.

- Real Estate: Using blockchain tech in real estate transactions streamlines verification and transfer of ownership, reducing paperwork and saving time. In turn, this makes real estate a more accessible and cost-effective industry.

- Secure Personal Information: Storing sensitive data on a blockchain offers heightened security against hacks. In turn, this enhances access control for industries like travel, healthcare, finance, and education.

- Voting: With personal identity information stored on a blockchain, voting becomes more secure, preventing double voting and tampering. Blockchain technology therefore simplifies the voting process, increasing accessibility and decreasing election costs.

- Government Benefits: Digital identities on a blockchain can streamline the administration of government benefits, to reduce fraud and operational costs. Beneficiaries can also receive funds faster through digital disbursement on the blockchain.

- Medical Information Sharing: Storing medical records on a blockchain ensures accurate and up-to-date information. This system also improves things by speeding up record retrieval, which benefits both patients and healthcare professionals.

- Artist Royalties: Blockchain technology tracks digital files, ensuring fair compensation for artists. It also combats piracy and offers transparency through smart contracts for streaming services, guaranteeing that artists receive their rightful payments.

- Non-Fungible Tokens (NFTs): NFTs, represented as digital tokens on the blockchain, grant ownership of unique digital or physical assets. Here, NFT applications range from digital art to property deeds.

- Logistics and Supply Chain Tracking: Companies like Walmart and Maersk are already using blockchain tech to enhance logistics and supply chains. They’re doing this by storing unalterable data on secure public ledgers, which in turn, allows partners to communicate more efficiently.

The Future of Blockchain Technology

Current Trends and Developments

Here are some current trends and developments that are shaping the future of blockchain technology and its applications across society:

- The Rise of Decentralised Finance (DeFi)

As referenced throughout this article, DeFi is a system of financial services that operates on blockchain networks and smart contracts, allowing users to access lending, borrowing, trading, and investing without intermediaries or fees. Naturally, as blockchain technology adoption increases, so will the prevalence of DeFi.

- Non-Fungible Tokens (NFTs)

Through representing ownership of various forms of art, collectables, gaming items, and more, NFTs offer a new way of monetizing and verifying digital creativity. As blockchain technology becomes more integrated into day-to-day life, so will the concept of real-life ownership being depicted through NFTs.

- Blockchain as a Service (BaaS)

BaaS is a business model that allows blockchain developers to use cloud-based platforms to create and host superior blockchain applications and smart contracts.

Challenges and Solutions

Like other emerging technologies, blockchain tech is also facing some challenges:

Scalability Issues

Blockchain networks have limited capacity and speed to process the chain of transactions and data. This can result in high transaction fee, congestion, and delays for users and applications.

Some solutions to this issue are Layer-2 protocols and off-chain solutions that increase the throughput and efficiency of blockchain networks, such as the Lightning Network for Bitcoin, and Polygon for Ethereum.

Likewise, the Ethereum Duncan Upgrade is another significant improvement attempting to enhance the scalability and efficiency of the Ethereum blockchain.

Interoperability Issues

Another major issue is the lack of compatibility and communication between different blockchain platforms and systems. Intuitively, this can limit the exchange of information and value across various networks and applications.

To address these concerns, various cross-chain bridges have been created, such as Ren, which connects Bitcoin with Ethereum and Polkadot.

Regulatory Issues

Regulatory issues refer to the uncertainty and inconsistency of blockchain and cryptocurrency related rules and regulations, especially across different jurisdictions.

Further, different KYC (Know Your Customer) and AML (Anti Money Laundering) laws in different geographies can create challenges and risks for users, developers, and investors in terms of compliance, taxation, and enforcement.

To solve these issues, industry leaders are resorting to self-regulation and collaboration – with self-regulation referring to the adoption of common standards and best practices, whilst collaboration leads to greater engagement and dialogue between regulators and policymakers.

The Blockchain Trilemma

The Blockchain Trilemma is a concept that highlights the trade-offs between three key attributes of blockchain networks: security, scalability, and decentralization. According to this theory, it is challenging for a blockchain network to simultaneously achieve all three feats at their highest levels.

- Security: Security refers to protecting data and assets on the blockchain network from unauthorized access, tampering, and attacks. A highly secure blockchain network is essential to maintain trust and integrity among users.

- Scalability: Scalability is the ability of a blockchain network to handle a large number of transactions quickly and efficiently. As mentioned earlier, scalability issues can lead to congestion and delays on the network.

- Decentralization: Decentralization is the distribution of power and control across nodes in a blockchain network. A decentralized network is more resilient to censorship, manipulation, and single points of failure.

Different solutions have been proposed to solve the Blockchain trilemma. Some focus on implementing changes at Layer-1 level, while others propose utilizing tools on top of the Layer-2s.

The reality is that there is no way to have a secure, scalable, and decentralized blockchain at the same time. One of these has to be sacrificed.

Blockchain Technology Explained – FAQs

What is the purpose of blockchain technology?

The purpose of blockchain technology is to provide a secure and decentralized method for recording and verifying transactions or data. This system eliminates the need for intermediaries and central authorities, thereby increasing transparency and reducing the risk of fraud or manipulation.

Trust and security issues have traditionally hindered digital transactions. However, the tech’s decentralized nature and secure cryptographic techniques offer a new approach to building trust and ensuring data integrity in a digital environment.

What are the benefits of blockchains over traditional finance?

Blockchains offer increased transparency, reduced transaction costs, faster transaction times, and enhanced security without the need for intermediaries.

What is the difference between a database and a blockchain?

A database is a centralized system managed by a central authority, while a blockchain is decentralized and records data in blocks that are chained together and secured using cryptography.

What are the 3 Pillars of Blockchain Technology?

The three pillars of blockchain are decentralization (no single point of control), transparency (each transaction is visible to all participants), and immutability (once data is added, it cannot be changed).

How is blockchain different from the cloud?

Cloud computing involves storing and processing data on remote servers accessed via the internet, managed by third parties. On the contrary, blockchains are distributed ledger technologies wherein data is stored across a decentralized network of computers.

Is blockchain technology secure?

Yes, blockchain is considered highly secure due to its cryptographic hashing and the decentralized nature that makes tampering with data extremely difficult.

What is the blockchain used for?

Blockchain tech is used for a variety of applications beyond cryptocurrencies, such as securing medical records, facilitating supply chain transparency, and ensuring the integrity of voting systems.

Where is blockchain technology used in real life?

Blockchain tech is used in real life for supply chain management, financial services, healthcare (for maintaining patient records securely), real estate (for property transactions), and more.

What is the difference between a blockchain and Bitcoin?

Blockchain tech enables the existence of cryptocurrencies, among other applications, by providing a decentralized ledger for transactions. Bitcoin is the first and most well-known cryptocurrency that operates on blockchain technology.

Can blockchains be hacked?

Yes. While blockchain technology offers enhanced security features due to its decentralized nature and cryptographic algorithms, it is not entirely immune to attacks. However, the risk of hacking is significantly lower compared to traditional centralized systems.

What is a blockchain audit?

A blockchain audit involves reviewing and verifying the security protocols, code, and functionalities of a blockchain implementation, to ensure it is secure against vulnerabilities, performs as expected, and complies with relevant regulations and standards. This is typically done by cybersecurity experts or specialized blockchain audit firms.